A skeptic’s view of nuclear energy

This paper, while skeptical of the robust nuclear renaissance many in the nuclear industry now predict, is not anti-nuclear. Indeed, nuclear power has many attractions. It is a mature and well-established technology, unlike, for example, carbon capture and storage. Improvements in its operation and reliability in recent years have been striking. It produces little carbon dioxide and can clearly, in principle, play a significant role in combating global warming. Compared to coal-generated electricity in particular, it is relatively clean, producing almost no emissions. Its energy output is not intermittent, as is the case with wind and solar. And though the overall costs of nuclear are rising, they are arguably competitive with other low-greenhouse-gas electric-generation alternatives.1

However, despite these many attractions, nuclear power seems to go forward only where governments heavily subsidize its operation, such as in China and India today. As Henry Sokolski has pointed out, “No private bank has yet chosen to fully finance a new nuclear reactor build; no private insurer has yet chosen to insure a nuclear plant against third party off-site damages.”2 In the United States, almost all of the several nuclear plants that are now being considered for future deployment are in states with regulated utilities, where nuclear does not have to compete directly with other generation sources and where rate payers in the state assume much of any risk. Nuclear power growth is stagnant or negative in most of the industrialized countries, and there is still today, outside of China and India, almost no nuclear power in the developing countries. In 2007, world nuclear electricity generation dropped by 2 percent; in 2008, for the first time in nuclear power’s history, no new reactor was connected to the grid anywhere. This should all give one pause in dreaming of a nuclear renaissance.

Several factors are pulling back on efforts to expand nuclear power: the very high capital costs inherent in nuclear power, especially given the large size of reactors driven by economies of scale; a continuing strong aversion to nuclear power by skeptical publics concerned with safety, with unresolved questions on how to handle radioactive wastes, and with the risks of nuclear proliferation, despite some recent improvements in favorability ratings; and the rise of renewable energy and other competitors for low-carbon electric generation.

The most striking aspect of nuclear power projections is the tremendous uncertainty about how rapidly or not nuclear capacity will grow worldwide over the next four decades. For example, the Nuclear Energy Outlook 2008 by the Nuclear Energy Agency of the Organisation for Economic Co-operation and Development (OECD) shows low and high scenarios as follows: the high scenario grows to about 600 GW by 2030 and then rapidly grows to almost 1,500 GWby 2050; the low scenario shows no growth to 2030 and then modest growth to 600 GW by 2050. The regional uncertainties are even more marked. For example, for OECD countries in North America, the range of change from 2004 to 2050 is 20 to 275 GW; for OECD countries in Europe, it is -10 to 200 GW; and even for China the range is considerable: roughly 60 to 120 GW.3 As noted below, the Nuclear Energy Agency’s projections for China, even to 2030, may understate the real range of uncertainty.

The high scenario assumes that carbon capture and storage proves not to be very successful; that energy from renewable sources is at the lower end of expectations; that there is early good experience with construction of new nuclear power plants; that carbon trading schemes are widely introduced; and that there is an increased level of public and political acceptance of nuclear power. The low scenario assumes mostly the opposite.4

On these points, the trends are mixed. Though there are some beginnings, there are still few substantial efforts underway to demonstrate carbon capture and storage. And while so far there has been no adoption of carbon trading systems outside of Europe, there is a growing expectation that some kind of cap-and-trade or carbon taxing system will eventually be imposed in the United States and elsewhere. On the other hand, renewables are expanding rapidly everywhere; the experience with new nuclear construction has not been good; and public acceptance of growth in nuclear power still appears low. In addition, the price tag for nuclear reactors is high and getting more marked.

The World Energy Outlook 2008 reference scenario shows global nuclear capacity growing from 368 GW in 2006 to 433 GW in 2030, with a preponderance of this growth in India and China. Russia also had ambitious plans for expansion, but recently announced a sharp adjustment downward.5 Growth in the United States, OECD countries in Europe, and in the developing countries is projected to be flat at best.

In the United States, despite many recent government incentives and reforms to speed up the regulatory process, there have been no firm orders for new nuclear plants. However, several utilities have filed combined construction and operating license applications with the Nuclear Regulatory Commission (NRC), which is now reviewing the applications; and four of the utilities have signed Engineering, Procurement, and Construction (EPC) contracts in anticipation of NRC approval. Most of the license applications have come from utilities in regulated markets, where risks are borne by rate and tax payers, though at least two have been submitted by merchant utilities.6 The lesser interest in nuclear in unregulated markets, where the risks are borne by competing market players, is not hard to understand. In a competitive market, the construction of a new nuclear power plant could represent a tremendous risk, as noted, for example, in the May 2008 report from Moody Investors Service.7

Nuclear capacity in the European OECD countries has been on a plateau for a decade, although construction recently began on two reactor projects, the Olkiluoto-3 plant in Finland and the Flamanville-3 reactor in France, both featuring the AREVA Evolutionary Power Reactor. The Olkiluoto-3 project started in 2005 and is now, by all accounts, three years behind schedule and already more than $2 billion over budget.8 Construction of the Flamanville-3 reactor started in December 2007, and it is too early to see if it will improve on the Olkiluoto performance.

José Goldemberg’s essay in this issue points to the several factors that militate against nuclear power in developing countries. For one, nuclear power plants, unlike dams and other infrastructure, are not underwritten by the World Bank or most other international lending organizations. The large investments required for nuclear power therefore compete with the pressing needs for health, education, and poverty reduction. Nuclear energy is also not included in the Kyoto Protocol mechanisms under which the industrialized (Annex 1) states can obtain credits against their own greenhouse gas emissions by investing in reducing emissions from developing countries.9 Second, with economies of nuclear scale continuing to push reactors to 1 GW size or larger, the grids in many developing countries simply cannot accommodate the reactors. And third, while the largest and more advanced of the developing countries do have economies and grids that could accommodate nuclear power, several, perhaps most, of these countries, Goldemberg emphasizes, have more attractive alternatives, including still largely untapped resources of hydropower and natural gas.

The striking exceptions to the tepid projected growth of nuclear power and the great range of uncertainty are the remarkable projections for India and especially China. In its reference scenario, the World Energy Outlook 2008 projects that by 2030 China will install an additional 30 GW of nuclear – substantial to be sure, but not unprecedented compared to past nuclear growth in other countries. Some recent statements by Chinese authorities, however, indicate much greater growth. In May 2007, China’s National Development and Reform Commission announced that its target nuclear generation capacity for 2030 is 120 to 160 GW! In June 2008, the China Electrical Council projected 60 GW of nuclear capacity by 2020!10 I do not know how realistic these recent projections are; but it is important to note also that the reference scenario of the World Energy Outlook 2008, while projecting an additional 30 GW nuclear capacity in China by 2030, also projects an additional 800 GW of coal capacity for the same period, which I will say more about later.

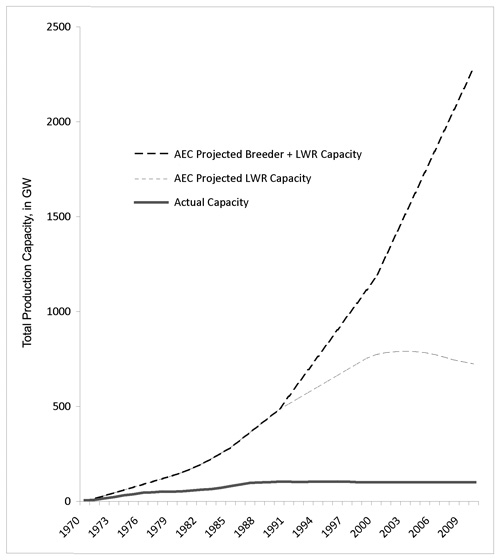

In some respects, the grand Chinese projections mirror those made in the United States in the 1970s (see Figure 1). There are differences to be sure: the U.S. projections were based on very high rates of growth of electricity – roughly twice the rate of GDP growth – while the Chinese electric growth rates assumed are closer to the GDP rates. Nevertheless, the 1970s projections by the United States do represent a cautionary tale of over exuberance, and it may be worthwhile to keep them in mind when evaluating China’s plans.

Figure 1

The U.S. Atomic Energy Commission Projection of the Growth of Nuclear Power in the United States, 1974

LWR stands for light water reactor, and Breeder refers to liquid metal fast [neutron] breeder reactor (IMFBR). Source: U.S. Atomic Energy Commission, Proposed Environmental Impact Statement on the Liquid Metal Fast Breeder Reactor (WASH-1535), 1974.

The fairly tepid projections for nuclear power outside of Asia are due to several factors, but two are particularly significant: the extraordinarily high capital investment required, and the continued public wariness about nuclear power, driven by an amalgam of concerns over safety, radioactive waste disposal, and nuclear proliferation.

The recent literature shows a range of costs both for nuclear and its competitors. For nuclear, overnight capital costs projected for new plants range roughly from $3,000 to $5,000/kW, with costs in the United States somewhat on the higher side.11 When total bus-bar costs are considered, nuclear appears at least arguably competitive with integrated gasification combined cycle coal (IGCC) and combined cycle gas turbine (CCGT) plants, if there is a carbon charge roughly in the range of $30 to $50 per ton of CO2 emitted. Nuclear also appears reasonably competitive with wind in many regions where the wind is supplemented by compressed air storage to make the wind resource more resemblant of base load.12

For the United States, the Energy Information Administration estimates the overnight cost of an advanced nuclear plant to be $3,300/kW,13 which would imply a capital cost, including interest paid during construction, of something like $4,200/kW. This, however, could be on the low side for plants constructed in the United States, at least as noted below.

Overnight costs for all forms of electric generation have grown over the past few years; but the rise in costs is especially significant for nuclear both because of the large sizes of new nuclear reactors and because the construction period for nuclear is markedly longer than for its principal competitors, thus adding to the total capital cost. Although there have been some paper studies of smaller reactors in the range of 50 to 100 MW, there are few plans to build and widely deploy such reactors. Also, while China and India are deploying small reactors, on the order of 300 GW, and some of these could, in principle, be exported to other countries, the market niches for such reactors appear limited. Studies of high-temperature gas-cooled reactors also contemplate a 100 to 300 MW scale; but none of these reactors is ready to go through the licensing process. Therefore, the new proposed reactors are, for the most part, 1 GW or considerably larger. Also, the principal reactors that are ready to deploy are all light water reactors.14

Thus, for example, in a March 2008 filing by Progress Energy with the Florida Public Service Commission, the company estimated the overnight costs for two proposed Westinghouse AP-000 Reactors (about 1,100 MW each) to be more than $5,000/kW for the first and $3,300/kW for the second. Including project escalation, escalated costs before AFUDC (Allowance for Funds Used During Construction), and AFUDC, the totals came to $8.3 billion and $5.8 billion, respectively, for the two reactors15 – a tremendous risk for any company or utility. In light of this risk, the credit rating company Standard & Poor’s points out that “no utility will commit to a project as large and risky as a new nuclear plant without assurance of cost recovery.”16 The World Energy Outlook 2008 makes a similar point:

In the traditional, vertically integrated public service model, the supply company was often a monopoly and could count on recovering the investment and the target return. . . . In the competitive situation now existing in most OECD countries and several non-OECD countries, risks have, to some extent, moved from rate and tax payers to competing market players. This perception of increased risk drives up the investor’s required rate of return.17

The risks evident in new nuclear construction are compounded by the prospect that the already longer construction period needed for nuclear compared to its competitors could be extended further still, both by public interventions and also by another problem associated with nuclear, if not unique to it: an erosion of construction and operating competence and lack of manufacturing infrastructure due to the almost complete absence of new builds in the United States and Europe over the past many years. If there were a real renaissance, these deficiencies would right themselves over time, with students again going into nuclear engineering, workers again being trained, and so on; but the current lack is certainly one reason for caution in assuming that such a renaissance will happen in the first place.18

Simply to replace retired nuclear capacity will require building a large number of new nuclear plants in the coming decades – a challenge given the continuing public skepticism about nuclear power. An opinion poll of 18 countries in 2005, sponsored by the International Atomic Energy Agency (IAEA), found that less than one-third of the public supported building new reactors. Even when prompted specifically about the possible use of nuclear energy to combat climate change, only 38 percent expressed support for an expanded reliance on nuclear power. It should also be noted, however, that more than two-thirds of those polled opposed shutting down nuclear altogether.19 Also, in some countries, including the United States, the United Kingdom, and Sweden, public acceptance of nuclear appears to be rising, though there are still sizable minorities strongly opposed.20

Public skepticism has been driven largely by worries about safety and radioactive waste disposal. Modern nuclear reactors have impressive safety features, and the new designs incorporate still further refinements. Nevertheless, the potential of a catastrophic event (either an accident or some kind of terrorist incident) is always present, and lingering concerns over safety certainly color public views of nuclear power. Aside from the immediate devastation that would be caused by a severe event, it is also widely recognized that were such an event to occur, the entire nuclear enterprise worldwide would be called into question.

Even if the chance of a severe accident were, say, one in a million per reactor year, a future nuclear capacity of 1,000 reactors worldwide would be faced with a 1 percent chance of such an accident each 10-year period – low perhaps, but not negligible considering the consequences.21 And it is worth emphasizing that while accident probabilities can perhaps be estimated, there is no real or persuasive way to gauge the risk of terrorist attacks on reactors. Until reactors are inherently safe – that is, until there is no credible way in which large amounts of radioactivity could ever be released – the specter of a catastrophic event will hang over the nuclear enterprise.

It is clear also that the unsettled state of radioactive waste disposal remains a component in public worry about nuclear power. Technically, waste disposal might not be an unsolvable problem. In the short term, dry cask storage appears relatively inexpensive and safe; in the long term, geological storage in a repository appears doable and safe. However, politically, solutions are not so easily come by. In the United States, this has been recently highlighted by the apparent demise of the Yucca Mountain repository.22 While Finland and Sweden (at the moment at least) appear to have found a political path to siting a repository, there has been little progress elsewhere in locating and developing repositories.

One final shadow over a nuclear renaissance is the growing international concern about nuclear proliferation. It is well understood that one of the factors leading several countries now without nuclear power programs to express interest in nuclear power is the foundation that such programs could give them to develop weapons. In this sense, the connection between nuclear power and nuclear weapons could lead to some expansion of nuclear power. But this motive would likely lead, at most, to very modest programs. The nuclear proliferation risk is instead more likely to inhibit nuclear expansion. For one, proliferation worries will surely restrict the amount of encouragement and subsidies that the large industrialized countries will be willing to extend to countries to develop nuclear power.

Certainly if a nuclear renaissance means spreading nuclear power to a score or more of new countries as well as expanding existing programs, then the current governance of the nuclear fuel cycle internationally would have to be much altered, with limits, for example, on national enrichment and reprocessing plants, were there a serious attempt to make nuclear expansion proliferation resistant. Such changes are possible but so far have garnered little support from countries that do not already have national fuel-cycle facilities in operation.

The strongest impulse to a nuclear renaissance is the view that nuclear represents the most developed and economic low-carbon electricity alternative.23 Other articles in this issue examine nuclear economics in more detail, but let it be granted that nuclear power will be roughly competitive with IGCC coal and CCGT gas if a carbon charge of something like $30 to $50 per ton CO2-equivalent is imposed. Though perhaps more controversial, let it also be granted that wind, combined with compressed air energy storage, will also be roughly competitive with nuclear. Leaving out other possibilities, such as solar and geothermal, among renewables, and end-use efficiency advances, the principal low-carbon alternatives to nuclear are likely to be carbon capture and storage at coal plants; natural gas combined cycle plants (even without carbon capture and storage); wind, both with accompanying storage and as a standalone intermittent source of electricity; and efficiencies in electricity generation.24 If we then ask which of these alternatives can give the world the biggest greenhouse-gas abatement for the buck, it is not at all clear that nuclear will look as indispensable to climate change policy as its proponents insist. Considering the limited amount of capital available for investment in electric generation overall, investment in nuclear plants could hurt the growth of potentially more effective alternatives.

The World Energy Outlook 2008 reports that carbon capture and storage (CCS) is “a promising technology for carbon abatement, even though it has not yet been applied to large-scale power generation.” A few CCS projects are under way and several full-scale CCS projects have been announced, varying in scale from industrial prototypes to projects on a 1,200 MWscale, with target dates for deployment between 2010 and 2017.25 Scientists appear reasonably confident that these projects will confirm that CCS could be competitive with other major carbon mitigation strategies, and that the geological CO2 storage capacity worldwide would be vast – sufficient to handle CO2 emissions from fossil-fuel plants for a century or longer.26 The U.S. Energy Information Agency, for example, estimates that, for an integrated coal-gasification combined cycle plant (IGCC) with CCS, the overnight cost is just over $3,000/kW, about the same as an advanced nuclear plant, assuming both come on line by 2016 and that the IGCC plant has a construction time two years shorter than the nuclear plant.27 It is too soon to rely confidently on CCS, but if it does develop as projected, it will be a close competitor to nuclear, probably with similar life-cycle costs and carbon abatement potential.

CCGT natural gas plants, of course, are not carbon free. However, even without carbon capture and storage, if they are replacing coal plants, they will save carbon emissions. A nuclear plant replacing a modern coal plant of 1,000 MW capacity would save about 1.5 million tons of carbon per year; a gas plant replacing the same coal plant would save about half of this, or 0.75 million tons of carbon per year.28 So the nuclear plant would double the savings. However, a modern gas plant has a capital cost about one-fourth that of a nuclear plant,29 meaning that for the same capital cost, natural gas could save more than two times the carbon emissions than nuclear! And it could do this far more quickly than possible with a nuclear expansion. Cumulative carbon saved over decades could be far greater than with nuclear.

If a large expansion in gas-generated electricity led to a more rapid rise in the price of natural gas, the greenhouse gas savings might not be worth the cost. But there have been many recent discoveries of natural gas in the United States and elsewhere; in fact, the natural gas resource worldwide appears to be much greater than had been estimated. In addition, a large expansion of wind, as described in further detail below, could release a considerable quantity of gas now being used for base-load generation – as well as substitute more directly for nuclear generation.

While installed capacity of nuclear has been roughly constant worldwide over the past decade, wind capacity has grown dramatically. At the end of 2007, cumulative world wind capacity was more than 94 GW, having grown at an average of more than 25 percent per year for the preceding eight years. In the United States, there have been no new orders of nuclear plants for more than 30 years. By contrast, in 2007, about 8 GW of new wind capacity were installed, with a cumulative capacity at the end of the year of about 17 GW.30 It appears that another 8 GW or more were installed in 2008. In 2008, the United States Department of Energy completed a study showing the feasibility of a scenario in which wind would contribute 20 percent of total U.S. electricity by 2030; such a contribution would require a wind capacity of about 300 GW.31Wind of course is an intermittent source of electricity generation, and its full exploitation will require more new transmission lines than would nuclear, because the strongest wind resources in many parts of the world (including in the United States) are far from demand centers. Nevertheless, wind economics look attractive.

On a capital cost comparison, wind turbines cost about one-half that of nuclear per installed kilowatt;32 since the capacity factor for wind might be one half that of nuclear, the carbon savings per capital cost for wind and nuclear might be roughly comparable. But, again, because wind turbines can be installed much faster than could nuclear, the cumulative greenhouse gas savings per capital invested appear likely to be greater for wind.

The wind projections heretofore have been mainly for stand-alone wind turbines without any significant storage. If recent estimates of the potential of compressed air storage prove on target, wind could eventually become a baseload resource, with a still greater upside capacity.

One other potent competitor to nuclear (and to CCS and renewable, too) will be efficiency improvements, both end-state and in the power sector itself. Here I look briefly only at the power sector. Today the world average fuel-to-electricity conversion efficiency of coal-fired power plants is below 35 per- cent.33 New coal-fired plants have efficiencies up to 46 percent, and by 2030 the efficiencies of a modern coal plant could reach 50 percent or higher. In its “business as usual” scenario, the World Energy Outlook 2008 estimated that worldwide coal generating capacity will roughly double from 2006 to 2030, with an overall average efficiency in 2030 of about 37 to 38 percent (41 percent in OECD countries).34 Investments that would drive the average efficiency of world coal-fired plants in 2030 from, say, 37 percent to 42 percent would save roughly the same amount of carbon emissions as would replacing 50 percent-efficient coal-fired power plants with 300 GW of nuclear power plants operating at a 90 percent capacity factor.35

At a national level, the average efficiency, in 2004, of China’s 307 GW of coal-fired plants was 23 percent.36 By 2030, the World Energy Outlook 2008 projects an overall efficiency of roughly 35.6 percent. If this could be raised to 41 percent for the 1,332 GW of coal-fired capacity that China is expected to have on line by 2030, that would save more than four times as much carbon emission on the same basis as would the 36 GW of nuclear capacity that the International Energy Agency expects China to deploy by 2030.37

As I initially noted, my analysis is not intended to make a case against nuclear power. The balance of arguments for and against nuclear – on economic, safety, environmental, and other grounds – is examined in the companion articles in this issue. What I have wanted to express is a strong cautionary note to the confident projections of an inevitable nuclear renaissance. In particular, it is important to realize the reasons why nuclear power is largely level or declining in most of the world, outside of Asia, and to underscore that this situation may not reverse, even in the face of the climate change challenge.

ENDNOTES

3 Nuclear Energy Outlook 2008 (Nuclear Energy Agency, 2008), 105.

5 Uranium Intelligence Weekly, March 9, 2009, 5.

7 Reported in “Nuclear Renaissance: U.S.A.” (NUKEM, June 2008).

8 “Olkiluoto-3 losses to reach 1.7 billion Euros,” World Nuclear News, February 26, 2009.

17 World Energy Outlook 2008 (International Energy Agency, 2008), 155.

18 See, for example, Schneider and Froggatt, World Nuclear Industry Status Report 2007, 12–13.

20 See Climate Change and Nuclear Power 2008, 39.

22 The Obama administration’s budget policy statement from March 10, 2009 (available at www.whitehouse.gov/omb) noted that “the Yucca Mountain program will be scaled back to those costs necessary to answer inquiries from the Nuclear Regulatory Commission, while the Administration devises a new strategy toward nuclear waste disposal.” It might be worth pointing out that the Waste Isolation Pilot Plant (WIPP) in New Mexico was sited without the political furor that has surrounded Yucca Mountain; possibly this was due in part to the fact that this plant is devoted to transuranic wastes and does not contain high-level radioactive wastes.

23 See Climate Change and Nuclear Power 2008.

25 World Energy Outlook 2008, 150.

27 Electricity Market Module, Table 8.2.

31 20% Wind Energy by 2030 (U.S. Department of Energy, July 2008).

32 Electricity Market Module, Table 8.2.