Appendix V: Back-End Concepts

Concept #1: Multilateral Arrangement for Emerging Nuclear Power Programs101

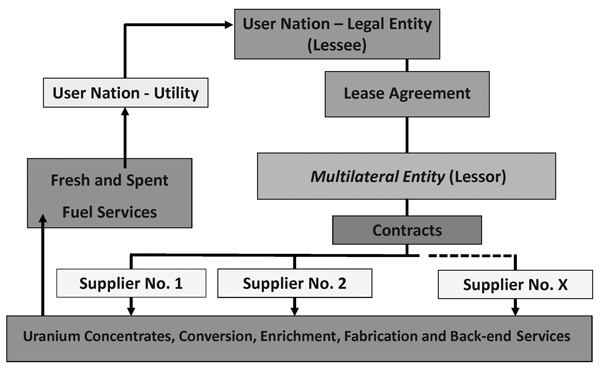

The two key players in a multilateral arrangement are the multilateral entity (lessor) and the user nation (lessee), in the form of a special purpose entity (SPE)102 (see Figure 2). Nuclear fuel leasing and nuclear fuel banks have recently been touted as workable mechanisms to facilitate agreements for providing what have often been called “cradle to grave” fuel cycle services to utilities that are only “consumers” of nuclear fuel. While implementation could vary widely, in one possible scenario a service provider or broker might arrange for the delivery of fresh fuel and the acceptance of used fuel at a centralized/regional interim storage facility and at a specified time following its discharge from the utility’s reactor. This type of arrangement would enable small nuclear fuel users to obtain fuel supply and disposition services at competitive prices (see Figure 2).

Figure 2. Multilateral Fuel Lease Arrangement

User nation denotes a consumer state. Source: Adapted from James Malone, James Glasgow, Stephen Goldberg, and Peter Heine, “TRUST, An Innovative Nuclear Fuel Leasing Arrangement,” NEI-WNA International Nuclear Fuel Cycle Conference, Budapest, Hungary, April 2007. Figure © Stephen M. Goldberg and Robert Rosner.

U.S. utilities have long used lease arrangements through SPEs as a mechanism to finance their acquisition of equipment and nuclear fuel.103 In these leases, utilities arrange for a financial institution to act as a trustee under a trust agreement between the utility and the lending bank.104 Some leases involve a “heat supply contract” with the trustee, whereby the trustee agrees to buy the fuel, lease it to the utility, and base the “rent” payment to the lessor on the heat generated through the use of the fuel in the utility’s reactor.105 As these lease arrangements mature, some utilities have been able to dispense with the need to obtain letters of credit in connection with such transactions.106 Other U.S. utilities have developed their own special financial arrangements to address their cash flow requirements.107

To the extent that states are able, under their national laws, to commit themselves to issue export licenses and grant retransfer approvals needed to establish meaningful long-term fuel supply assurances, those assurances should be incorporated in peaceful nuclear cooperation agreements that provide the legal framework for international nuclear commerce. To bolster governmental attempts to convince emerging state recipients of the binding nature of fuel assurance (assuming faithful performance of the agreement by the recipient), such agreements should incorporate an advance long-term programmatic assurance allowing the fuel and fuel components to be exported and retransferred for processing, and ultimately shipped to the intended destination. Nuclear fuel leases negotiated among private-sector participants should benefit from such assurances to the same extent as the governments under whose agreements for cooperation such commerce is carried out.

This approach offers the following advantages:

- In the long term, it could provide the financial and institutional support to develop, construct, and operate interim centralized and/or regional storage facilities.

- It could provide reliable fuel supplies buttressed by competitive pricing necessary for a viable commercial nuclear fuel industry.

- With regard to the front-end, such an arrangement could increase risk protection by mitigating the consequences of a fuel supply interruption for either physical or political reasons. Historically, states have managed this risk by maintaining large inventories. While prices for uranium and its attendant services (enrichment, conversion, and fabrication) have risen, and while it is becoming more expensive to dedicate capital to maintain inventory, fuel cost is a weak argument for sovereign (national) enrichment programs. The opportunity for diversification of supply that is inherent in the proposed fuel supply model provides an alternative to maintaining large inventories as a way to manage the risks of supply disruption; and it remains effective regardless of the cost of carrying inventory.

- It could provide a hedge against likely cost increases for front- and back-end services.

- By pledging the revenues from electricity sales, it could facilitate the payment for infrastructure projects in the developing states; and it reduces the capital formation requirements of these states. We understand that the interest rate to finance such projects is significantly higher than commercially issued sovereign debt. Even if developing states were able to obtain lower concession rates from international development entities, the blended rates would not be substantially lower.108 Therefore, the cost of borrowing capital to pay for nuclear fuel for entities in the developing world is substantial. In addition, some investment banks have suggested that binding contracts for supply of the nuclear fuel required by the plant over a substantial portion of its life would be a necessary condition for financing the construction of new nuclear power stations.

This approach offers the following disadvantages:

- It would likely require significant start-up capital.

- It would likely revert to a scheme that puts more emphasis on conventional reprocessing and recycling. In our general opinion, user or consumer states will put a value on the used fuel and will eventually want to burn the recycled MOX fuel.

- It would require multiple bilateral and multilateral agreements and commitments, likely calling for a new institutional entity to manage the leasing arrangements.

- It would likely require protracted discussions to iron out all the contract and payment terms. The discussions may take so long that by the time the agreements are ready to be implemented, consumer states may have already locked themselves into fuel supply and conventional reprocessing contracts.

Concept #2: A Linear Model— A Special Case for the Multilateral Fuel Lease Arrangement

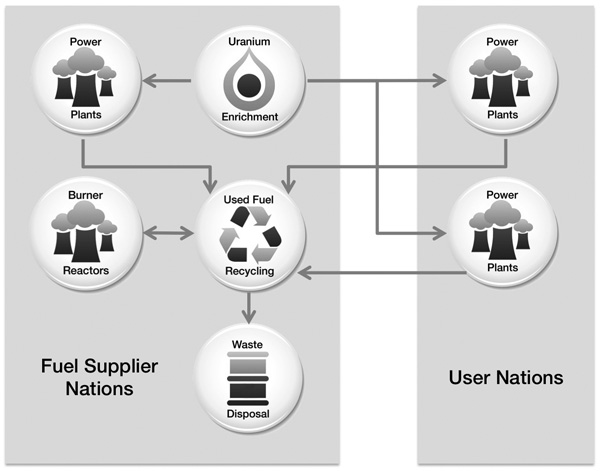

An alternative model that has received some attention is the linear model; in this case, a “bundled fuel supplier” (AREVA) offers bundled services, including conventional reprocessing and recycling services (Figure 3). This bilateral approach is more readily adapted to the current fuel supply regime.

This approach offers the following advantages:

- Start-up capital would likely not be a barrier to implementing this model.

- It could encourage aspiring consumer states to make deals with existing suppliers, which can supply fuel cycle services with “economies of scale.”

- It could discourage developing states from building individual enrichment and conventional reprocessing facilities, provided that all services are available. (For example, if local waste disposal is not available, waste would be returned.)

- It could require significantly less effort in negotiating a fuel regime framework because it typically involves a much smaller number of critical partners; indeed, it can be viewed as a relatively modest evolution of the existing, already viable fuel supply network.

- This approach offers the following disadvantages:

- It would indirectly encourage adding conventional reprocessing capacity.109 The likely outcome is a short- to intermediate-term increase in the stocks of civilian separated plutonium.

- It is not conducive to a flexible technology (including advanced chemical partitioning, if proliferation-resistant) and final disposal opportunities. Thus, it will prematurely shut off choices on advanced technology opportunities.

Figure 3. A Linear Model

User nations denotes consumer states and fuel supplier nations denotes fuel supplier states. Source: Modified from Stephen Goldberg and James Laidler, “Financial Strategies for Future Reprocessing Facilities,” World Nuclear Fuel Cycle Conference, April 6, 2006. Reprinted with permission from the World Nuclear Fuel Cycle.

Industry representatives’ favorable view of the linear model is understandable, as industry would not want to perturb (any more than necessary) the existing viable fuel supply network. Furthermore, one can see how preserving the existing industry contractual agreements would best serve regional storage arrangements.

ENDNOTES

To help ensure that the lessor’s remedies can be effectively enforced in the event of the lessee’s default, the lessor could require that the lessee be in a state that is a party to the Hague Convention on the Recognition and Enforcement of Foreign Judgments in Civil and Commercial Matters or (for leases that specify arbitration), the New York Convention on the Recognition and Enforcement of Foreign Arbitral Awards. The efficacy of such remedies, coupled with recipient government guarantees, has been demonstrated by experience with the project finance agreement for fossil-fired generating stations and other industrial facilities in developing states.

Under existing U.S. law, any U.S. fuel assurance will be subject to the need for the U.S. government, as well as private-sector suppliers, to obtain an export license from the U.S. Nuclear Regulatory Commission, an independent regulatory body. Congress and the U.S. executive branch are likely, in any fuel assurance agreements, to retain the authority to refuse to perform U.S. supply assurances, even for reasons that are unrelated to any concerns about the recipient state’s faithful performance of its nuclear nonproliferation commitments. Numerous judicial decisions and fundamental principles of U.S. constitutional law compel a conclusion that, regardless of whether U.S governmental supply assurances contain the usual “subject to U.S. law” phraseology, those supply commitments will yield to any subsequent law enacted by Congress and to any regulation or executive branch order as well; such regulations and orders are part of U.S. law. In light of U.S. practice for many decades, such supply commitments are likely to contain a “subject to U.S. law clause.” Moreover, the U.S. government, in accordance with its past practice in connection with substantive U.S. commitments in treaties and other international agreements, may insist on a broad right of the United States to terminate those commitments, without being in breach of any legal obligation.

108. Paul K. Freeman et al., “Infrastructure in Developing Countries: Risk and Protection,” International Institute for Applied Systems Analysis, http://www.iiasa.ac.at/Research/RMS/june99/papers/pflug1.pdf.