The Growth of Global Commercial Interests

The underdeveloped rules for space security became a more pressing problem as rapid advances in information technology made space a more valuable arena and as space technology spread beyond the Cold War powers and their allies to developing countries and commercial firms. By the early 1990s, basic trends led many observers to predict that global commercial activities would soon replace national military programs as the dominant feature shaping space security. Although these predictions eventually proved to be overly optimistic, they played an important role in shaping policy debates and decisions about space security in the 1990s.

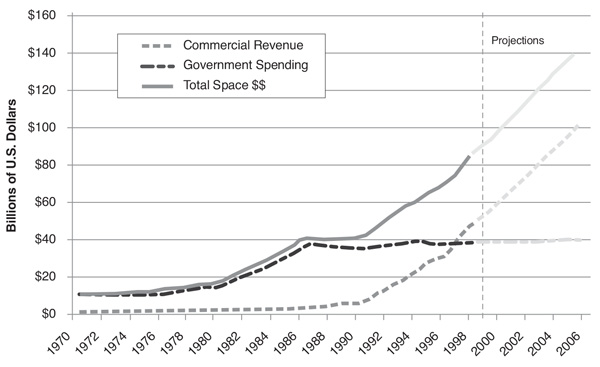

American and Russian firms with space expertise began looking for new business opportunities after the end of the Cold War and severe cutbacks in the Soviet space program removed the competitive rationale for the high levels of government spending on missile defense and space weapons research initiated during the Reagan years. Exponential advances in computing capabilities to handle large amounts of data generated optimistic forecasts for broadband communications satellites in geostationary orbit (GEO), while improvements in miniaturization and lightweight composite materials made constellations of small satellites in low earth orbit (LEO) look like a safe and cost-effective way to provide mobile telephone services.35 As the global economy became increasingly interconnected and knowledge-driven, commercial demand for remote imagery, precision timing and navigation signals, and satellite launch services was also expected to surge. Annual global commercial space revenues, which had inched up to $6 billion by 1990, surpassed government spending on space in 1997, and were projected to reach $100 billion by 2005, while government spending was expected to stay flat (Figure 1).

Figure 1: Projections for Commercial Space Industry Surpassing Government Spending

Source: Futron, Satellite Industry Guide, 1999–2000 (October 1999): 1, 11.

Whereas space development and infrastructure costs historically had been borne by governments, industry began to invest a significant amount of private capital in developing new space technologies. Iridium, an off-shoot of Motorola, anticipated that business travelers would be willing to pay handsomely for mobile phones that would work anywhere in the world. The company raised billions of dollars in private financing and overcame a number of technical and manufacturing challenges to mass produce and launch a constellation of 66 satellites over a two-year period—an unprecedented feat because satellites and launch rockets typically were custom built and mated, a process that normally took several years.36 The Orbital Sciences Corporation offered another example of industry innovation when it used off-the-shelf and relatively inexpensive subsystems and software to develop a way to launch small satellites from aircraft rather than from dedicated sites on the ground.37 Industry analysts anticipated a virtuous cycle in which commercial firms using private funds for space projects would be highly motivated to reduce their costs, improve their products, and protect their investments, thus making space an increasingly attractive venue for additional commercial ventures.38

In anticipation of this projected trend, the U.S. government changed a number of space-related rules to encourage global commercial activity. After the 1986 Space Shuttle Challenger accident, the Reagan administration stopped using the shuttle for commercial payloads. To increase the number of launch options available for U.S. commercial satellites, the Reagan, George H. W. Bush, and Clinton administrations negotiated bilateral agreements with China (1988), Russia (1993), and the Ukraine (1996) to provide launch services at rates that would not be too far below those offered by U.S. firms trying to get back into the commercial launch business.39 To facilitate overseas satellite sales, presidents Bush and Clinton transferred responsibility for communications satellite export control decisions from the State Department, which regulates foreign sales of munitions, to the more business-friendly Department of Commerce, which regulates foreign sales of dual-use goods.40 In 1994, Presidential Decision Directive 23 authorized private firms to begin selling high-resolution satellites and imagery so that U.S. companies could compete with Russian, French, and future foreign firms for an annual satellite imagery market that was predicted to reach between $2 billion and $20 billion by 2000.41 The United States and Russia also agreed to cooperate on the International Space Station (ISS), partly to keep Russia from selling some rocket technology to India and partly so that Russian expertise in extended human space flight could reduce the cost of a U.S. project that was in danger of cancellation.42 The 1995 formation of Sea Launch— a joint venture among Boeing, the Russian and Ukrainian makers of the relatively inexpensive and highly reliable Zenit rocket, and a Norwegian shipping firm—marked the first entirely private effort to manufacture and launch satellites and symbolized the financial advantages of global space cooperation.

In arguing for rule changes to facilitate commercial space activities, proponents did not claim that the economic benefits outweighed the negative effects on national security. Rather, they suggested that the end of the Cold War and the effects of globalization fundamentally altered security calculations so that some types of cooperation could serve both objectives. If the primary nuclear threat to U.S. security was proliferation rather than Soviet aggression, then both economic and security benefits would flow from cooperative space projects that used former Soviet military equipment and scientists for peaceful purposes and that strengthened Russia’s nonproliferation capabilities and commitments.43 If most death and destruction was now caused by civil conflict, humanitarian crises, or environmental catastrophes rather than massive cross-border aggression, then making commercial satellite imagery readily available to all interested states, as well as to intergovernmental bodies and NGOs, would increase transparency and facilitate equitable management of security problems that no one country could handle on its own.44 If a number of other countries and private companies were now willing to sell advanced satellites, launch services, and space-based information products, then the United States would be hurting itself economically for no national security gain if it kept tight export controls on items that could be indigenously produced or acquired elsewhere in the global marketplace. Finally, if U.S. firms had a dominant position in a rapidly expanding commercial space industry, many future military needs could be met through competitively priced commercial services, per-satellite launch costs could be reduced by spreading fixed costs over more users, and companies could invest more of their own revenue in researching and developing new products rather than expecting the government to pay a large share of research-and-development costs.45

Despite these emerging considerations, traditional security concerns still impeded some space-related commerce and cooperation, such as early efforts to end the deliberate degradation of GPS signals.46 By the time the full GPS system became operational in 1995, the number of nonmilitary GPS users had already surpassed military users because GPS receivers had become inexpensive and easy to use alone or in combination with satellite imagery, wireless communications, the Internet, and sophisticated desktop computer software. In hopes of preventing its enemies from using free GPS signals to get accurate location information, the United States was degrading the open signal while giving its own military users an encryption key to eliminate the distortion. A 1995 National Academy of Sciences’ study found that this “selective availability” (SA) policy imposed burdens on legitimate GPS users without enhancing U.S. security because commercially available differential GPS technology could correct for the distortions. The study suggested that removing SA would eliminate the expense of differential GPS for commercial and civilian users, encourage more effective and widespread use of GPS technology, reduce incentives to use undegraded signals from Russia’s version of GPS, the Global’naya Navigatsionnaya Sputnikovaya Sistema (GLONASS), and protect GPS’s position as the international standard for global satellite navigation systems.47 A RAND study done at the same time placed more emphasis on military concerns that turning off SA during peacetime would make it politically difficult to restore SA during wartime and that turning off SA would encourage the faster spread of GPS technologies to potential adversaries, thus reducing the advantage enjoyed by the U.S. military.48 The Clinton administration decided to continue the SA policy until 2000—by which time the U.S. military was more adept at jamming GPS signals over a localized area. This delay strengthened European resolve to develop their own precision timing and navigation system, Galileo, in order to avoid dependence on the U.S. military for a service that seemed increasingly vital to economic development and human security. As expected, ending GPS signal degradation gave a huge boost to commercial use, and the ratio of nonmilitary to military users quickly reached 100 to 1.49

Impressive growth in commercial space activity during the 1990s led to predictions that the world was entering a “second space age” that would be shaped more by market forces and a “merchant” culture than by large-scale government projects undertaken by members of the “guardian” culture for national prestige and deterrence stability.50 In the late 1990s, though, neither group was clearly dominant: indeed, many Clinton-era space policy debates reflected these different communities’ conflicting ideas about managing the global spread of dual-use technologies. The increasing number of space users had little experience working across commercial, civilian, and military lines within their own country, let alone negotiating with merchants and guardians from other countries that now had a direct stake in issues such as the allocation of orbital slots and radio-frequency spectrum or the use of satellite imagery in crisis situations.

Failure to agree on new operating rules became increasingly problematic under the emerging circumstances. A 1995 National Research Council report warned that orbital debris posed a growing threat to individual satellites and might make entire orbits unusable unless all space-faring nations quickly agreed on debris reduction measures and data exchanges.51 Many observers expected the case for more inclusive and effective governance of space as a “global commons” to become ever more compelling as the value of space- based communications, imagery, weather forecasting, and navigation services surged and space played an integral, if invisible, role in many other information-age activities, such as operating electrical power grids and validating credit-card transactions.

But as these optimistic predictions were peaking, developments that invalidated them were already underway. The information technology bubble burst in the late 1990s, and projected demand for broadband and other satellite communications services—the major source of profit in space—failed to materialize after exuberant investors chasing those projections had developed communications satellite constellations and fiber-optic landlines well in excess of actual market demand.52 A similar story of disappointed expectations occurred in the satellite imagery field.53 Demand for satellites and launch services also precipitously dropped just as new providers entered the international market.54 Major losses were incurred, investors were chastened, and a large amount of unutilized communications and launch capacity discouraged new initiatives. Recently, the strongest growth in the commercial space industry has come from direct-to-home television, video, and radio services provided by entertainment companies that neither think of them- selves as part of the commercial space industry nor pay attention to space security policy.55 With private investors compelled by market circumstance to be much more cautious, government contracts have determined research and development choices. A number of high-profile satellite start-up firms—the merchants who were once expected to reshape space culture—either went out of business or, as in the case of the Iridium LEO satellite communications system, ended commercial service and went to work for the military. For some indefinite period of time, the U.S. military will remain the principal source of investment in developing new space capabilities even as international commercial utilization of those capabilities creates broader constituencies.

ENDNOTES

38. Because satellites are extremely expensive pieces of equipment that travel through space beyond the jurisdiction of any individual state, satellite manufacturers, financiers, and operators have been particularly interested in having uniform international legal rules to protect their investments. The UN Institute for the Unification of Private Law (UNIDROIT) is developing a draft protocol on space property that will do for space vehicles what the 2001 Convention on International Interests in Mobile Equipment, also developed by UNIDROIT, does for trains, aircraft, and other high-value mobile equipment regularly moving across national frontiers in the ordinary course of business. (The convention went into effect in 2004 and is available at http://www.unidroit.org/english/conventions/mobile- equipment/main.htm.)

45. On the mutually reinforcing benefits of U.S. dominance in global commercial, civilian, and military uses of space, see John Pike, "American Control of Outer Space in the Third Millennium" (e-print, Federation of American Scientists, November 1998),http://www.fas.org/spp/eprint/space9811.htm.

46. GPS satellites broadcast two types of signals, the Standard Positioning Service (SPS or C/A-code) for general use and the Precision Positioning Service (PPS or Y-code) for military use. The United States began using SA in 1990 to deliberately degrade the location accuracy of SPS signals from 20 meters to 100 meters while giving military users encryption keys to eliminate the effects of SA. Differential GPS uses information from a reference station at a known location to compute correction factors that can be used to compensate for the effects of SA at other nearby locations. For an overview of GPS technology and policy in the 1990s, see Per Enge and Pratap Misra, "Introduction: Special Issue on Global Positioning System," Proceedings of the IEEE, 87, no. 1 (January 1999): 10,http://ieeexplore.ieee.org/iel4/5/15872/00736338.pdf.

47. Aeronautics and Space Engineering Board and the National Research Council, The Global Positioning System: A Shared National Asset (Washington, DC: National Academy Press, 1995), http://www.nap.edu/catalog.php?record_id=4920.

54. By 2001, ten-year forecasts for commercial satellite launch demand had dropped from the 1997 high-growth forecast of 85 payload launches per year to 45 payload launches per year, and even those projections proved overly optimistic. See the series of annual reports released by the Federal Aviation Administration, Office of Commercial Space Transportation and the Commercial Space Transportation Advisory Committee, Commercial Space Transportation Forecasts, http://www.faa.gov/library/reports/commercial_space/forecasts/.