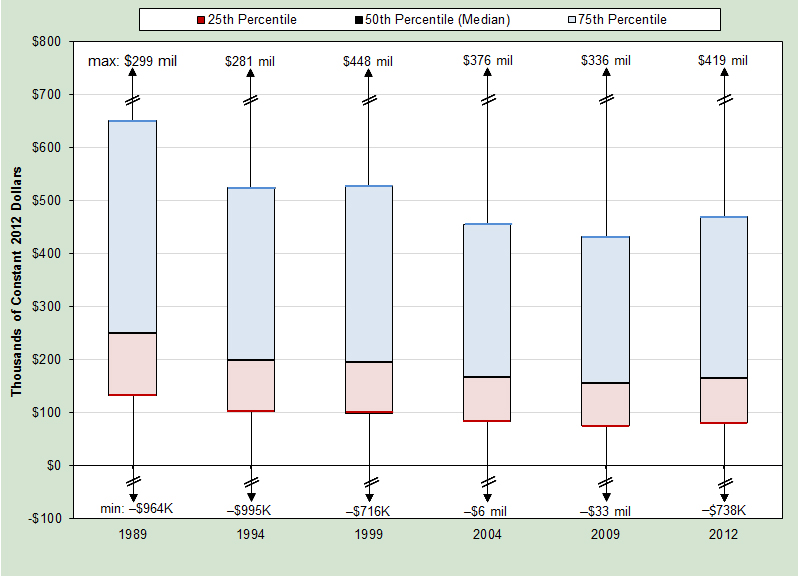

IV-20b: Range in Revenues of Not-for-Profit Humanities Organizations, 1989–2012* (Adjusted for Inflation)

* Organizations whose gross receipts were $50,000 or more. Years are “circa” years, a concept developed by the collector of these data to compensate for the often substantial lag between the end of organizations’ fiscal year and their filing of IRS Form 990, the annual financial report required of all public charities—and the source of the data presented in this indicator. For more on circa years and the rationale for excluding organizations with gross receipts of less than $50,000, see “About the Data.”

Source: Original analysis by the Humanities Indicators of data culled from the Internal Revenue Service Form 990 Return Transaction Files by the Urban Institute’s National Center for Charitable Statistics. Revenues were adjusted for inflation using the Gross Domestic Product Implicit Price Deflators produced by the U.S. Department of Commerce’s Bureau of Economic Analysis (annual deflators, vintage 3/27/2015; http://research.stlouisfed.org/fred2/series/ GDPDEF/downloaddata, accessed 4/6/2015).

The not-for-profit organizations that are the focus of this indicator are all IRS-designated 501(c)(3) public charities. As the IRS explains: “A private foundation is any domestic or foreign organization described in section 501(c)(3) of the Internal Revenue Code except for an organization referred to in section 509(a)(1), (2), (3), or (4). In effect, the definition divides section 501(c)(3) organizations into two classes: private foundations and public charities. Generally, organizations that are classified as public charities are those that . . .

- Have an active program of fundraising and receive contributions from many sources, including the general public, governmental agencies, corporations, private foundations or other public charities,

- Receive income from the conduct of activities in furtherance of the organization’s exempt purposes, or

- Actively function in a supporting relationship to one or more existing public charities.

Private foundations, in contrast, typically have a single major source of funding (usually gifts from one family or corporation rather than funding from many sources) and most have as their primary activity the making of grants to other charitable organizations and to individuals, rather than the direct operation of charitable programs” (http://www.irs.gov/Charities--Non-Profits/Charitable-Organizations/Public-Charities, accessed 5/29/2015).

The data that are the basis of the analysis presented here were culled by the Urban Institute’s National Center for Charitable Statistics (NCCS) from the IRS Form 990 Return Transaction Files. In the earlier years for which data are presented here—1989, 1994, 1999, and 2004—the IRS required that every tax-exempt public charity with typical gross receipts of $25,000 or more complete the Form 990 annually. Using the form, charities described their financial condition, activities, and key personnel. The IRS has since changed its rules with regard to which organizations must file and how much financial information they must provide. To ensure the comparability of data for earlier years with data for 2009 and 2012, the Humanities Indicators (HI) limited the updated analysis to organizations whose gross receipts were typically $50,000 or more.

In analyzing the information supplied by organizations on their Form 990s, the NCCS employs the National Taxonomy of Exempt Entities (NTEE), a widely used categorization scheme developed by NCCS to distinguish among the various kinds of organizations on the basis of their primary mission. While the NTEE includes a category for the humanities, other types of organizations that the HI consider to fall within this category, such as humanities-focused museums and libraries, are classified separately within the NTEE. In 2005, at the request of the HI’s data analysis team, the NCCS assembled information on all tax-exempt humanities organizations that fall within the HI’s purview* at five-year intervals going back as many years as the NCCS database permitted. This yielded data for a 15-year period extending from 1989 to 2004. The recent update of this indicator involved adding two data points (2009 and 2012) and also data for certain organizations that were not captured as part of the first analysis, including adult literacy organizations and heritage language schools.

The data presented here are for “circa” years, a concept developed by NCCS to compensate for the often substantial lag between the end of organizations’ fiscal year and their filing of IRS Form 990. The range of the circa year period includes fiscal periods starting in the most recent calendar year, plus the prior two calendar years.

* For an inventory of the kinds of institutions and groups considered “humanities organizations” for the purpose of this indicator, as well as examples of the types of organizations included in each of the broad categories of humanities organizations, see “What is a ‘Humanities Organization’?” The humanities not-for-profit sector as defined here does not include private not-for-profit general educational programs or institutions.